On June 29 at 4 p.m. EST (NY) we have our first summer book club of 2026 with JW (Josh) Mason on his new book with Arjun Jayadev, Against Money. We'll have a registration link soon but join the Discord or stay tuned.

Mona Ali's review says: "For Mason and Jayadev, real resources aren’t the fundamental constraints on productive activity; the capacity to make (monetary) promises is. Theirs is a radically capacious view."

This week we're looking at what we can or can't know about how energy demand changes once more hydrocarbon traffic is flowing through the Strait of Hormuz; and Europe's big about-face on defending its industries against Chinese exports; and how it now faces trade-offs not dissimilar to developing countries.

-Kate and Tim

The post-deal energy outlook

Ships are once again traveling out of the Persian Gulf through the Strait of Hormuz. The signing of an agreement between the U.S. and Iran at, er, Versailles is being cast by both sides of U.S. politics as a humiliation, but it means – questions of tolls and general capriciousness notwithstanding – an end to the bombing of civilians and infrastructure, as well as reduced odds of food price spikes, energy shortages, global recession, etc. And it seems to signal an end of American support for Israel's heinous attacks on Gaza and Southern Lebanon.

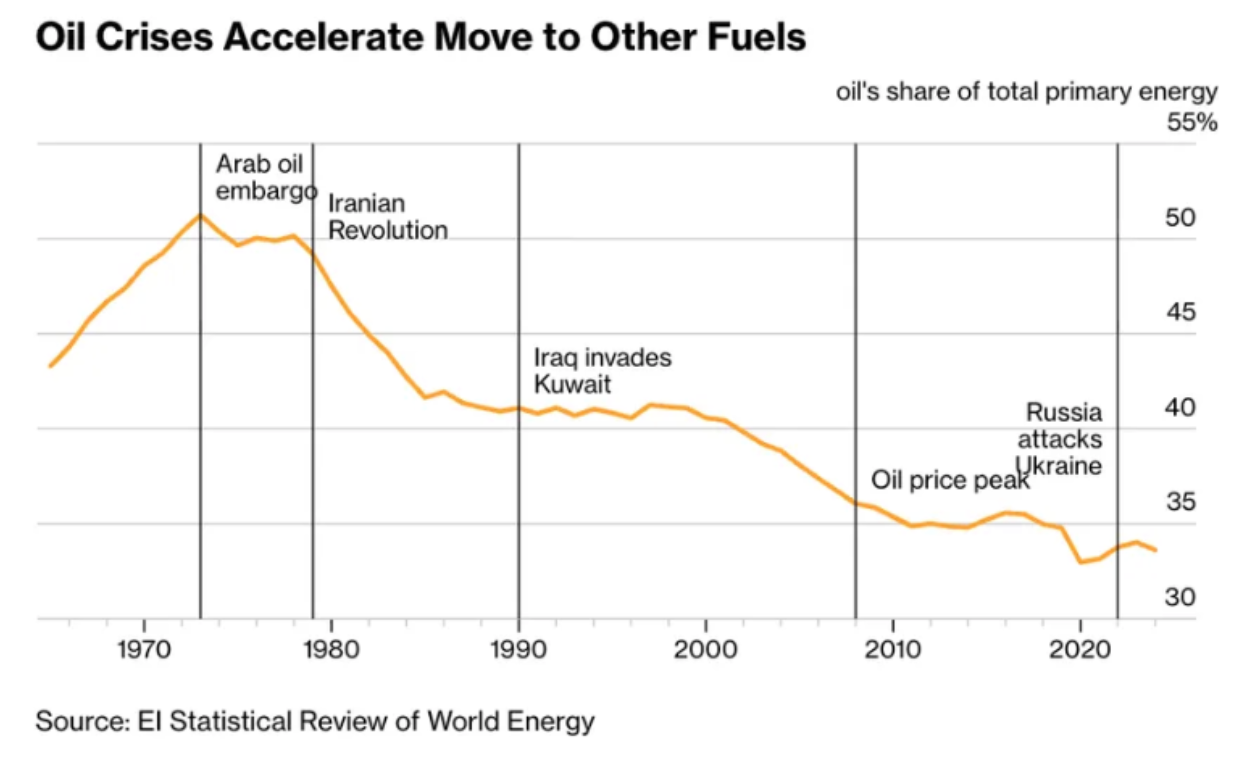

If the war on Iran has ended, it happened without ever pushing oil futures above their previous record of $147, let alone as high as the $200 mark that horrified energy analysts anticipated.

The mystery of why oil prices didn’t go as high as predicted is not so great: most of it can be accounted for by Chinese strategic reserves, other Strategic Petroleum Reserves including the U.S., enhanced pipeline throughput, accumulated storage at sea before you even get to counting demand-side measures.

Will the suppression of prices mean that demand for oil isn’t curtailed as much as it was after previous shocks, or to the degree that people like us might expect? Oil-oriented energy experts are drawing that conclusion already but it’s not a convincing argument. The global crude benchmarks don’t tell us that much about demand responses. The most-watched prices like Brent futures don’t reflect the amounts paid for actual deliveries of crude or refined products like diesel and jet fuel (Singaporean jet fuel, for example, famously rose far higher than Brent) – especially in Asia, where the shock hit hardest. Nor did they reflect the increases in the spot Liquefied Natural Gas (LNG) market or the fact that some LNG shipments just didn’t happen.

Estimating the quantitative effect of any of this will be difficult. Consumption of any type of energy is the outcome of multiple supply and demand-side factors. Indian manufacturer Mahindra is speeding up plans to expand its EV production capacity. LNG projects in Southeast Asia have been cancelled. Estimating the consumption effects of specific measures is possible, but assessing all decisions against a counterfactual of no war is tricky. It’s difficult to know how policymakers, firms and investors will make choices informed by the risk of this type of disruption recurring — and to what extent decisions might also reflect the rapidly changing economic and investment case, especially where solar + storage is an option. In a recent briefing, Rystad analysts noted that the demand destruction driven by the 1970s oil shocks was underestimated by forecasters at the time. It will be surprising if it can be accurately anticipated this time.

Does this mean Tim’s war thread will end? Stay tuned.

****

“China has decided not to import anything anymore”

Europe is panicking about the threat of Chinese manufacturing to its own industries to the extent that there is now unity between the biggest member states that something must be done.

Hedge funds are betting against the bonds of European carmakers because of China.

Germany is backing a French proposal to develop a new instrument to protect against Chinese imports and promote diversification of procurement; Poland and the Netherlands are also on board.

“We remain, by principle, in favour of free trade, of the WTO, but we are not naive any more,” the senior EU diplomat said. “If you read the five-year plan of China, it is . . . an attack on the market. China has decided not to import anything any more, and to subsidise overcapacity, dumping products on our markets.

[...]

The diplomats said rising unemployment and factory closures had hardened the mood across member states in recent weeks. However, there is still a reluctance to escalate in some capitals that are very open to Chinese investment and also fear Beijing's retaliation.

Reportedly the Centre for European Progress paper by Sander Toidoir and Brad Setser (which featured in our last essay about responses to China’s manufacturing) highlighting German complacency was helpful in getting Germany’s chancellor Merz on board with the French proposal. The paper points out that the country’s exports grew at twice the rate of global growth last year, but its imports stalled – widening the Chinese surplus with the rest of the world.

It’s hardly original to point out that Europe was too slow to respond to this. Even with more member state unity on the urgency of the problem, it’s not clear how Europe can effectively defend its own industries that are being quickly out-manufactured by Chinese counterparts. Trade barriers are short-term and prone to provoking retaliation. Industrial strategy is the better response, but it is complex and slow; China has been working on it for decades while most European leaders followed the promise of liberal globalisation.

While Europe begins to consider a new instrument, and is pushing along the proposed Industrial Accelerator Act, which would screen FDI and impose local content rules on publicly-funded procurement — the Commission itself might not have much say in it. Palma Polyak, a researcher at the Max Planck Institute for the Study of Societies, says that in fact much of Europe’s response to China’s new manufacturing surge has already been decided. Relaxation of state-aid rules after Covid-19 led to a doubling of national subsidies provided to industries since 2020; the amount spent by member states dwarfs what the EU would provide. During the same period, European climate policy became green industrial policy, which only added to the trade-offs that Polyak identifies. At a high level, these are: climate neutrality, industrial competitiveness, and strategic autonomy. But each of those contains more trade-offs.

The nature of the dilemma this creates for Europe is not very different from that faced by developing countries, she points out in her new paper:

“Long analyzed in debates on extractivism and postcolonial resource politics (Riofrancos 2017, Alami et al. 2025), as well as dependent development (Amsden 1989, Nölke and Vliegenthart 2009) – these conflicts have now migrated into the industrial core. Read in this light, Europe’s battery rollout serves as a cautionary case for green industrialization under conditions of asymmetric technological power, illustrating how difficult it is for latecomers to secure a favorable position in an emerging global “green division of labor” (Lachapelle et al. 2017) dominated by China. Europe’s internal divisions erode its capacity to act strategically in this global scramble.”

Indonesia’s nickel regime irks China

Some of the tensions described by Polyak can be seen in Indonesia’s relationship with China. Indonesia’s nickel export ban is one of the most inspiring examples for resource-rich developing countries and has led to considerable FDI from China into Indonesia, as we covered in the previous Dispatch. But in the past few weeks China has complained about new Indonesian regulations on nickel production, which they say restricts volumes and raises production costs. China’s Chamber of Commerce wrote a public letter complaining about the measures, while China’s embassy in Jakarta also wrote a private letter to President Prabowo. The challenge for Indonesia is that it wants to make more from its nickel resources; but relies heavily upon Chinese investment in onshore facilities through which it captures more of the value for its domestic economy.