A collaborative advantage

Bargaining chip watch: extractives edition

By Kate Mackenzie, Tim Sahay —

Bargaining chip watch: Extractive export bans

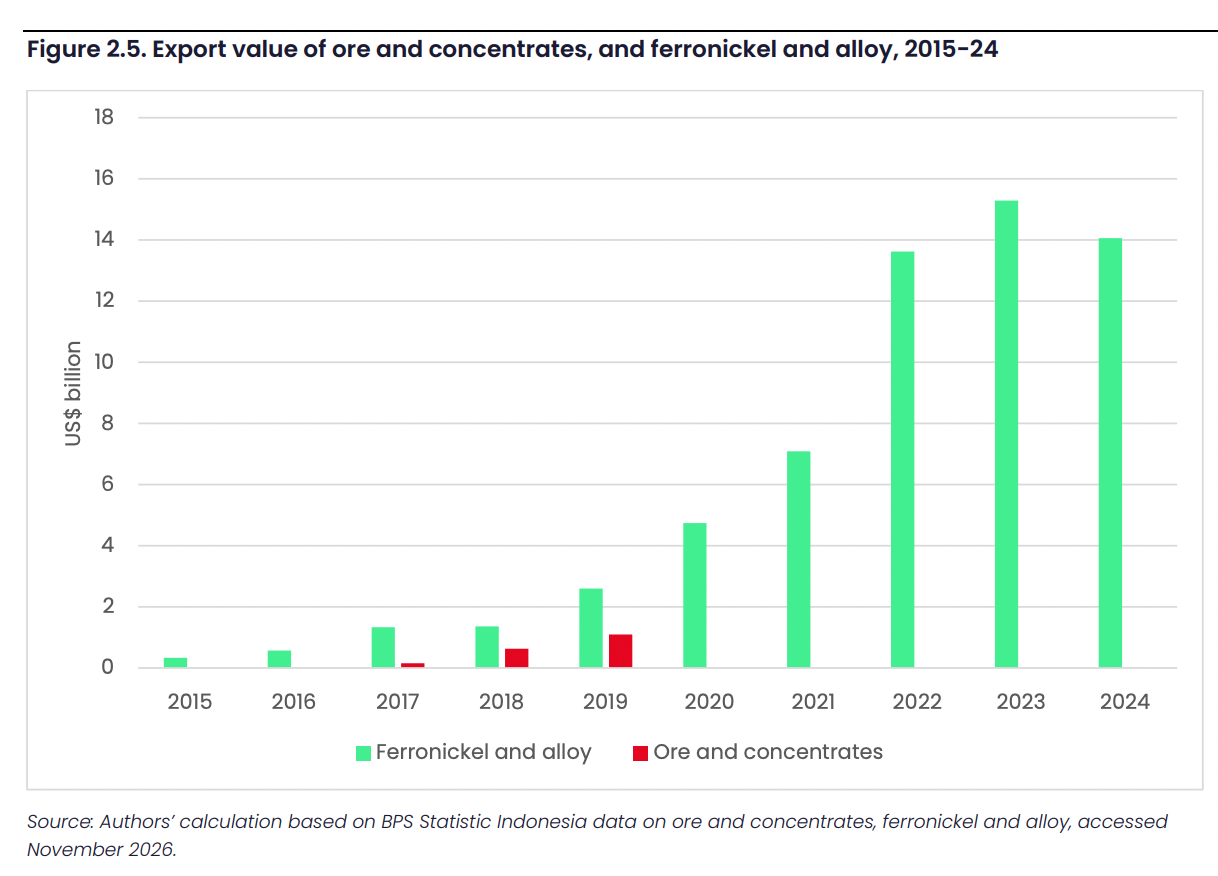

One of the most talked about initiatives by a developing country this decade is Indonesia’s decision to ban raw nickel exports. Nickel is (still) critical for a large portion of EV batteries, and for other tech such as mobile phones. Indonesia holds the world's largest nickel reserves; the idea of the export ban was to capture more of the nickel value chain in its own economy.

A report last month from CETEX at London School of Economics notes that the ban has indeed helped Indonesia to attract foreign direct investment (FDI) and improved the country’s trade balance since it went into effect in 2020. The two main nickel regions’ contribution to national GDP has also risen substantially.

Yet the report’s authors caution that the ban comes with environmental and social trade-offs, and that “while the export ban has allowed Indonesia to move along the nickel supply chain, it has also effectively created an oligopsony in which Chinese-Indonesian smelting consortia can dictate the market price and reduce the profit margins of mining companies in the country.”

Most countries are contending with multiple threats and constraints, including an increasingly hostile U.S., climate change, an energy and fertilizer market crisis, the open abandonment of international rules-based systems by powerful countries, the persistence of U.S. dollar centrality, and Chinese dominance across a large swathe of the manufacturing universe.

In the midst of these threats, several sub-Saharan African countries are following the Indonesian strategy, and using their mineral reserves to carve out development opportunities via similar export bans.

In May, the Chinese aluminium company, Chalco, announced a $1.2bn alumina plant in Guinea, with a 5% stake going to the government – plus an option to raise it to 35%. That announcement followed Guinea restricting exports of bauxite and seeking to onshore its processing into aluminium. Zimbabwe (lithium), the Democratic Republic of Congo (cobalt) and Namibia (lithium) have all imposed export limits or bans on minerals in the past three years.

Indonesia’s success is often cited as an inspiration for mineral-rich sub-Saharan African countries, and DRC officials last year proposed collaborating with Indonesia on the cobalt market (together they produce almost 90% of global output).

A paper from Africa Policy Research Institute by Eszter Szedlacsek and Rachmi Hertanti proposes something more concrete: the European Union could collaborate with Indonesia in developing African mineral supply chains. Indonesia, which is seeking to develop an EV battery industry, has signed MOUs around critical minerals and green tech with more than half a dozen African countries including Kenya, Morocco, DRC and Rwanda, and its state-owned enterprises have been investing in African partnerships.

Europe is trying to diversify its critical minerals supplies – mostly away from China – and the EU’s Critical Raw Materials Act commits to partnerships with alternative suppliers. The EU has also signed MOUs with several African countries. Emmanuel Macron attended a Franco-African summit in Nairobi last month, promising the continent’s governments that Europe’s adherence to free trade and rules-based international order made it a better partner than the U.S., China, or middle power countries like Russia and Turkiye. French or other European partners, he said, wouldn’t be “predatory” and could offer defense-industrial cooperation and innovation.

But Europe has little enthusiasm for certain strategies used in the Global South countries that want to use their mineral resources to develop; the EU lodged a successful WTO complaint about Indonesia’s 2020 nickel export bans. Szedlacsek and Hertanti write that the EU’s “financing structures and concrete project pipelines remain fragmented and vague. The EU’s approach, diverging from South-South cooperation, has also been critiqued for potentially reinforcing unequal ecological exchanges between the Global South and Global North.”

In contrast, Indonesia’s partnerships take place in the ‘Bandung Spirit’ of equality to keep downstream benefits in a supply chain within the Global South, and focus on capacity-building, knowledge transfer and value-added production in the CRM sector.

The Afripoli paper nevertheless argues that Indonesia and Europe could be complementary, as the latter offers technical expertise and Global South solidarity (Indonesian-African initiatives date back to Bandung) while Europe has financial power, regulatory expertise and considerable market access. It would be a kind of “collaborative advantage” of the South-North-South variety.

What to read

- Phenomenal World First Edition

Phenomenal World, our wonderful collaborators/editors and the publishers of our monthly essay, have re-launched with a new format; the first edition is on American Power.

“On the one hand, the United States appears as a waning hegemon, accelerating the transition away from its own unipolar era. On the other, each unprecedented shock reaffirms Washington’s unique privilege to directly reshape the world.”

Take a look at Eskandar Sadeghi-Boroujerdi on Iran’s resilience on the face of U.S.-Israel attacks; Catherine Schenk on the dollar’s dominance in historical perspective; and an interview by PW’s Maria Fernanda Sikorski and Jack Gross with Herman Mark Schwarz about his views on the U.S. empire.

- Common misconceptions about China green tech exports

The latest edition of the Caravanseri newsletter by Advait Arun, Daevan Mangalmurti and Aastha Uprety takes on the prompt of “Common misconceptions about Chinese clean tech exports.” The contributions cover the relative lack of success of Chinese nuclear exports; the slow recognition within India that China no longer only makes low-end goods; and that Chinese industrial success looks very different when it’s extended beyond green tech and to include industries where China has been less disruptive (pharmaceuticals) and less successful (aviation and advanced semiconductors).

- Geopolitically driven energy shocks accelerate electrification: Hormuz is to Asia what Ukraine was to Europe.

Akshat Rathi and several colleagues at Bloomberg wrote a data-driven piece on something we’ve been interested in for a while now: the extent to which geopolitically driven energy *shocks* change the world economy, and how much oil and gas demand destruction we can expect from this latest energy shock as nations race to electrify away their import vulnerabilities.

What Tim said in his interview with them was that the energy strategy of Europe and Asia from 1979 onwards was predicated on a fundamental assumption encoded in the U.S. 'Carter Doctrine': that the U.S. military would be the hegemon of the Persian Gulf. But in 2026, "Guys with speedboats and drones in Hormuz have ended American hegemony." And consequently, “Hydrocarbons have now entered a different risk regime, with the U.S. unable to guarantee stable supplies from the Middle East."