Dawn of the Electric World Order

Global shockwaves from the war on Iran are accelerating the energy transition

By Kate Mackenzie, Tim Sahay —

Oil and gas—the foundation of global systems of energy and production—are no longer reliably available where and when they are needed at bearable prices. Two wars in four years have triggered a permanent risk regime shift. No matter how uneven and uncertain the immediate reaction from markets and governments, the lesson of the present energy shock is unavoidable: the geopolitical conditions that once stabilized the carbon-based logistics of the modern world can no longer be guaranteed, and electrification offers a structural exit from instability.

After two months of war and supply chain disruption, the situation is becoming desperate in much of Asia and Africa, and roiling across Europe and the Americas. Many oil and gas importing countries are now being forced to triage: how much LNG goes to power generation versus fertilizer plants? Bidding wars will leave those without deep pockets paying in increased hunger, lost wages, and shrinking economies. It’s not just oil being affected by the war. From cooking gas to fertilizers to sulphur to helium, the war has yet again exposed the material underpinnings of the global economy and its web of interdependence.

Crises of this breadth and magnitude transform societies, firms, and governments. Societies boil under the strain of shortages, rationing, and hunger; economic distress cascades and political orders melt. After 2022’s inflationary shock, dozens of governments fell in a wave of anti-incumbency at the ballot box. Underlining the scale of the 2026 energy shock, IEA head Faith Birol said “More oil has been lost… than during the twin shocks of the 1970s that triggered recessions and fuel rationing around the world.” What will this crisis bring?

“A superior alternative”

What makes this shock different from the 1970s and 2022? As analysts at Ember put it: “this is the first energy shock with a superior alternative.”

In the more benign pre-shock landscape, mass electrification, solar and wind energy generation, and battery storage were already becoming competitive with fossil fuels. Electric vehicles accounted for about a quarter of all new car sales. Heat pumps and induction cooktops were growing in popularity. This combination of clean energy, storage, and electrification allow for countries to cut their dependence on a constant flow of imported fuels.

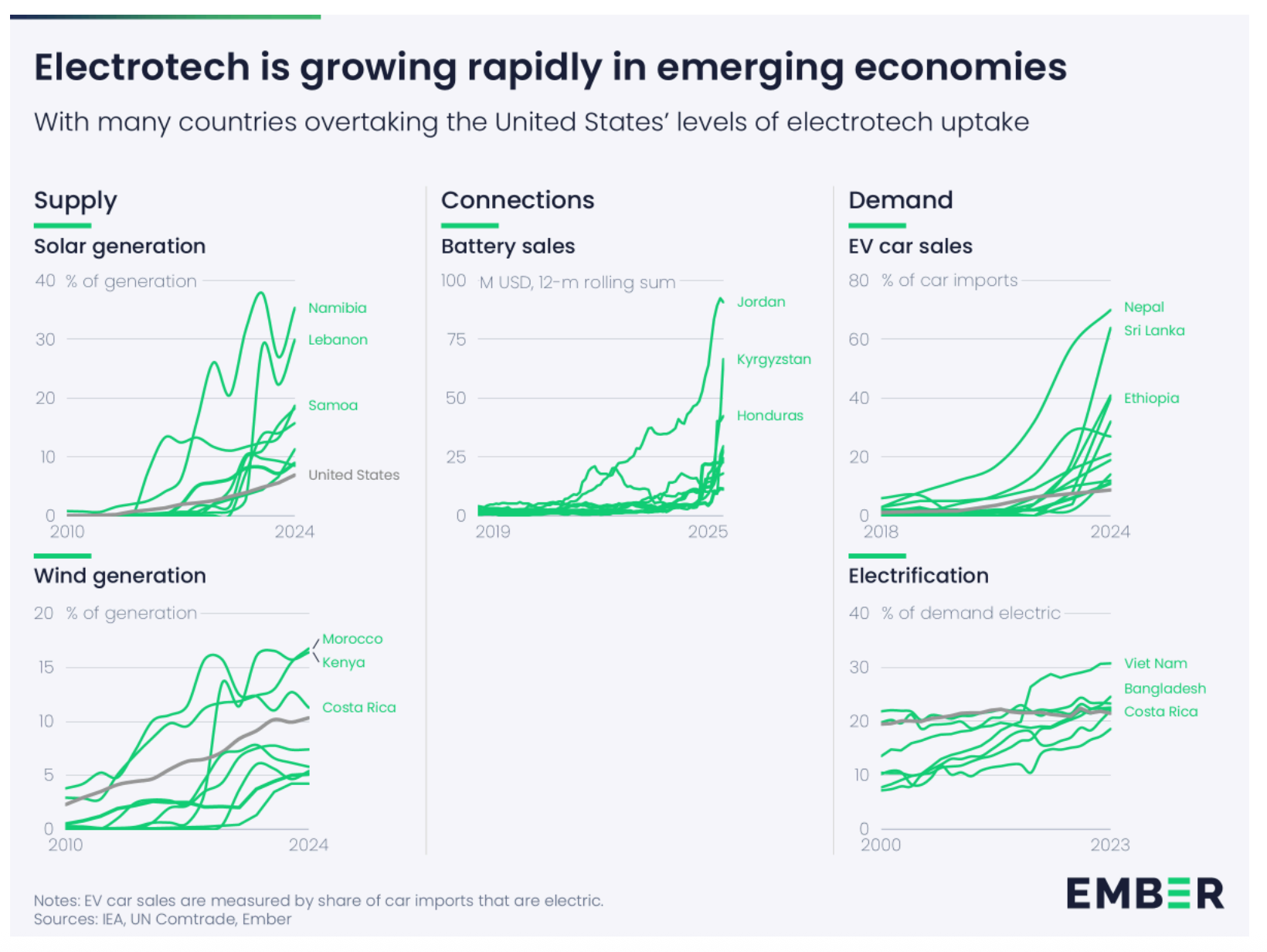

Even in 2022, when the Russian invasion of Ukraine put pressure on global oil and gas markets, electric vehicles and solar panels were less cheap than they are today. The rate of EV sales tripled between 2022 and 2025 and in the same period grid-scale storage grew almost tenfold to 270GW. Spain, Australia, and the UK have recently begun to see the peak prices of grid electricity subdued even in periods of huge demand surge, because renewable power and batteries are increasingly substituting for expensive gas-powered peaker plants. For any buyer not blocked by trade wars, renewable energy and storage technologies are mature, cheap, and accessible.

Once a climate project, electrification is now a geopolitical insurance policy. Seventy-five percent of the world’s population lives in net fossil fuel importing countries and collectively spends $1.7 trillion a year importing fuels. Many of those governments facing a loss of confidence in global oil and gas markets are expanding clean energy and electrification projects. In April, France announced $10 billion in subsidies for EVs and heat pumps. The month prior, Spain introduced measures to further speed up electrification, renewable generation, and storage. Vietnam is about to ban petrol motorbikes in downtown Hanoi and Ho Chi Minh City; the country’s giant conglomerate Vin is abandoning a planned LNG terminal in favor of a renewable project. Nigeria’s solar imports from China in March were more than five times the level of a year earlier. The list is endless.

Resilience and capacity

The new option of a “superior alternative” in energy security exists largely due to China, whose industrial policy and manufacturing prowess have made electrification cheaper, better, and more abundant. China’s factories today supply most of the solar panels sold around the world, most of the battery cells, and almost three-quarters of EVs.

China’s electrification drive was never primarily a climate story. It was a strategic imperative driven by energy security and industrial ambition. Beijing was spooked by the oil risks exposed after the 2003 Iraq War. The model was simple: build the clean industrial base at home to reduce reliance on imported fossil fuels, and then export that resilience.

The strategy produced the “electrotech” order of the 2020s. During the pandemic, China moved away from its debt-fueled infrastructure and property growth model to focus on the “new three”: batteries, solar photovoltaics, and EVs. The problem in the mid-2020s was not electrotech overcapacity, but a lack of coordinated global demand. The Hormuz shock has violently solved that under-demand problem.

Manufacturing factories for solar PV, wind, and batteries in China are only running at around half their capacity, meaning they can easily meet the surging global electrotech demand with the war. And manufacturing capacity has grown outside of China, too: Chinese electrotech firms have invested more than $210 billion in foreign solar, battery, and EV production facilities overseas since 2022. Since October, China has been selling more solar cells and other intermediate components than finished solar panels—as many countries want to make, and not just buy, panels.

Shock and awe

Big energy supply shocks spur fast energy transitions. More than climate conscious policy, financial upheaval, technological advances, or climate change-driven natural disasters, shocks to the energy system drive change in the energy system. Geopolitical catastrophe—war, blockades, embargoes—creates the supply-side shocks necessary for big changes in the energy complex to unfold.

The result of the Hormuz shock—now cascading through fertilizer, food, and critical industrial inputs like sulfur and helium—will be demand destruction for fossil fuel energy. Long-term reductions in demand will be joined by permanent substitution for the supply of energy from other sources. And this destruction will be largely state-led: most countries will cut their dependence on oil and gas if they can, although their available choices for doing so will vary.

States that already have momentum towards electrification will accelerate it. Spain has already benefited from a big solar and wind energy buildout over the last decade, with renewables providing more than 40 percent of its power. Madrid now views its cheap clean electricity as a way to attract energy-intensive industries away from gas-dependent European countries whose electricity prices have spiked yet again “Berlin and Paris,” argued Marc Lopez Plana in Agenda Publica, are now “viewing Spain as a competitor in the race to become the continent’s industrial core.”

Others will proceed in a more piecemeal way towards electrification and a more renewables-intensive system, even if they can only realize some of the benefits.

Meanwhile, states with powerful fossil fuel lobbies, or those that lack fiscal space, may see consumer-led energy transitions, while the state bears the legacy of stranded assets. This is the Pakistan scenario: the country spent several billion dollars a month importing LNG for its power generation, and suffered blackouts after the 2022 Ukraine invasion, while its LNG cargoes were being diverted to high-paying European customers. Households and businesses rapidly deployed their own solar panels and batteries at a staggering pace to produce the world’s fastest solar boom, effectively matching the country’s grid capacity. This has insulated parts of the population, to a degree, from the recent price spikes; it’s estimated to have saved 12 billion in LNG imports between 2022 and 2026 and save an additional $7 billion this year. But financial obligations remain a heavy burden in the form of take-or-pay contracts for coal and gas power generators that remain under-utilized and for servicing the debt used to build the facilities.

Consumers buying solar panels, induction cooktops, EVs, and heat pumps can have significant effects on oil and gas demand. Understanding the new risk calculus, consumers act as self-insurers—whether against blackouts or higher utility bills. In the UK, Octopus Energy reported heat pump orders doubling in a single month; EV and solar orders are rising worldwide. This is the hyperagency of consumers, outpacing policy or public investment and transforming energy systems. For most African countries, and some in Asia, the total capacity of privately owned diesel generator sets exceeds the installed grid power capacity. These are now being swapped for solar plus batteries. Policy makers need to recognize the world-shaping power of this demand, and harness it to upgrade grids and expand electrification.

Counterpoints

There are scenarios that could slow or constrain the shift—but each in turn has particular counterpressures that point towards an irreversible change. Inflationary pressures and reduced fiscal space can raise the cost of capital and hamper investment in clean energy. Asia’s reliance on coal—thus far providing only a small part of the response to the crisis—could grow. Regional wars could escalate into a world war; clean energy supply chains could break down. And extreme climate events can create yet more problems, especially for food; a large El Nino system looks increasingly likely. New emergencies will elicit new responses, not all of which are certain to point away from carbon.

For most countries, the new system has to be built while the old one is still operating. The difficult “mid-transition” issues will persist. For developing countries especially, financing costs and fiscal restraint will create drag. The disruption of other critical commodities such as fertilizers could add further strain on the current account of countries.

After the Ukraine invasion sent oil and gas prices soaring, there were predictions that Europe’s energy mix would become more fossil fuel-based, not less. But those predictions didn’t come true: renewable energy grew faster instead, and power from wind alone exceeded that generated by natural gas in 2024. Sales of European heat pumps doubled as residential heating was electrified by governments and consumers wanting to replace Russian gas.

Swimming against the tide, the US government is seeking to project global dominance of oil and LNG supply—proclaiming its hydrocarbons “geopolitically secure.” Will buyers get in line? While US sales of oil and LNG to Europe soared since the start of the war in Ukraine, few countries in 2026 are looking to increase their reliance on imports from the US. Earlier this year, the US ambassador to Europe threatened the loss of privilege to US LNG if it didn’t comply with the terms of a 15 percent US tariff “deal” struck last year.

Meanwhile, there are plenty of signs that Asian countries are moving decisively to cut dependence on imports—especially LNG—altogether. More than two dozen energy executives interviewed by Bloomberg journalists “painted a picture of a region that had been thought of as the future of LNG, but is now rapidly losing faith in the super-chilled fuel.”

There is also little sign of an increase in coal burning. Despite coal being possibly less vulnerable to chokepoints than natural gas, research by CREA finds the amount of thermal coal shipped in March was actually lower than a year earlier, even when shipments within large producers like Indonesia and China are included, and coal power generation was near flat.

Despite the White House’s energy dominance refrain, US oil companies do not plan to ramp up production on a scale that would compensate for the barrels taken offline in the war. Industry figures cite reluctance due to the lower prices of longer-dated oil futures, Trump’s assertions that he’ll keep gasoline prices low, or just general uncertainty. Oil industry participants in the Dallas Fed survey guessed that the amount of US oil being pumped will only increase by a quarter of a million barrels per day and at most half a million barrels by 2027—about a quarter to a half percentage point of world consumption.

In the short term, the war raises export income for US oil and gas producers. In the longer term, the energy dominance strategy is self-defeating—creating profound volatility, insecurity, and intermittency that militates against investors, consumers, and governments alike.

Within the United States itself it might be difficult to sense just how quickly the world is changing. Equities markets have been reaching record high levels; crude oil futures are nowhere near the crisis heights expected by energy experts. Renewables projects are being cancelled all over the country and EVs are not filling the streets.

Other rich fossil fuel exporting countries, from Norway to the UAE, have been diligently decarbonizing their energy systems for years. And for the last few years, many of the world’s poorest countries have been leapfrogging the age of fossil fuels with rapid uptake of solar panels and e-bikes. A carbon energy superpower, the United States looks increasingly like an energy island. Last year, we wrote that the central speculative question about US “fossil drenched” energy geopolitics was whether it would be forced “to watch as others climbed towards the solar uplands, or have the power to crush the spring.” This monumental energy supply shock sets the stage for that question to be answered. A fossil fuel supremacist government has made oil and gas costly and unreliable and accelerated the turn to the electric world order.